On Friday, Statistics Canada released new sector-level Gross Domestic Product (GDP) for June 2020. After much speculation, this data offers an idea of how Canada’s recovery from the COVID-19 economic crisis is likely to unfold.

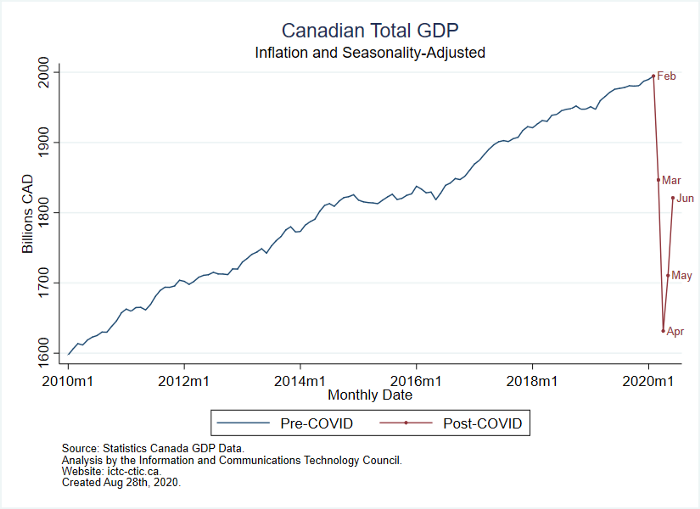

In short, the resumption of economic activity has been faster than many analysts expected. This relief comes after months of record-breaking plunges in economic indicators. Figure 1 below shows that aggregate Canadian GDP in June had nearly recovered to the level of March 2020, just following the onset of the pandemic, and was about 9% below the February peak.

Figure 1: Canadian GDP, Adjusted for Inflation and Seasonality

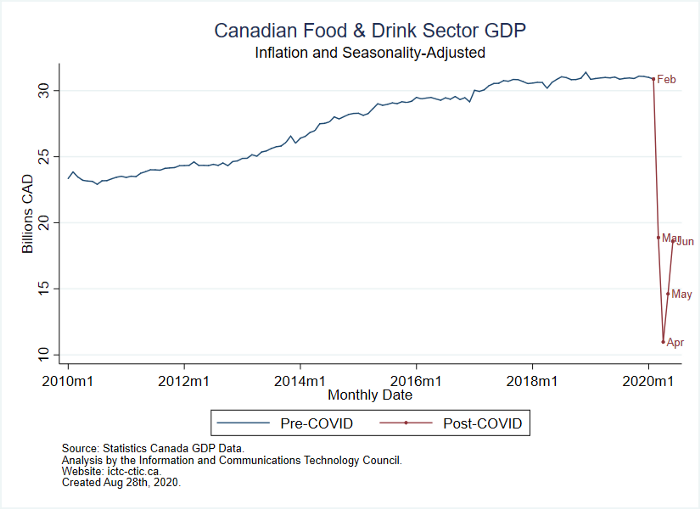

Some sectors continue to struggle, particularly Food & Drinks. Figure 2 reveals that the sector remains about 40% below its February level.

Figure 2: Food and Drinks Sector GDP, Canada

Construction industry GDP has largely bounced back, as shown in Figure 3.

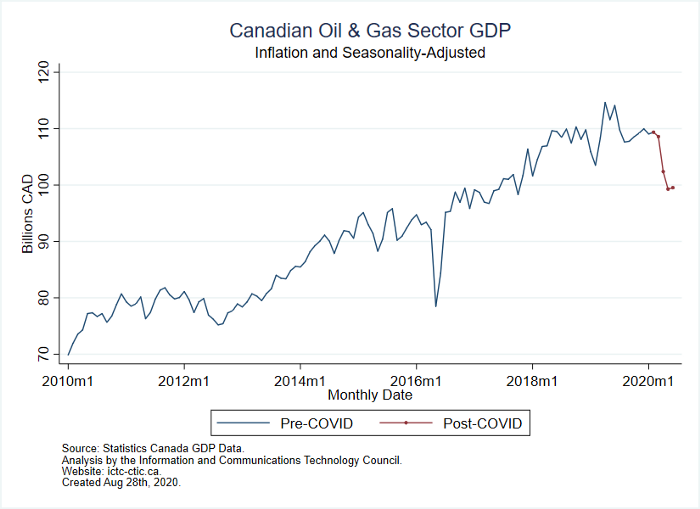

Figure 4: Oil & Gas GDP, Canada

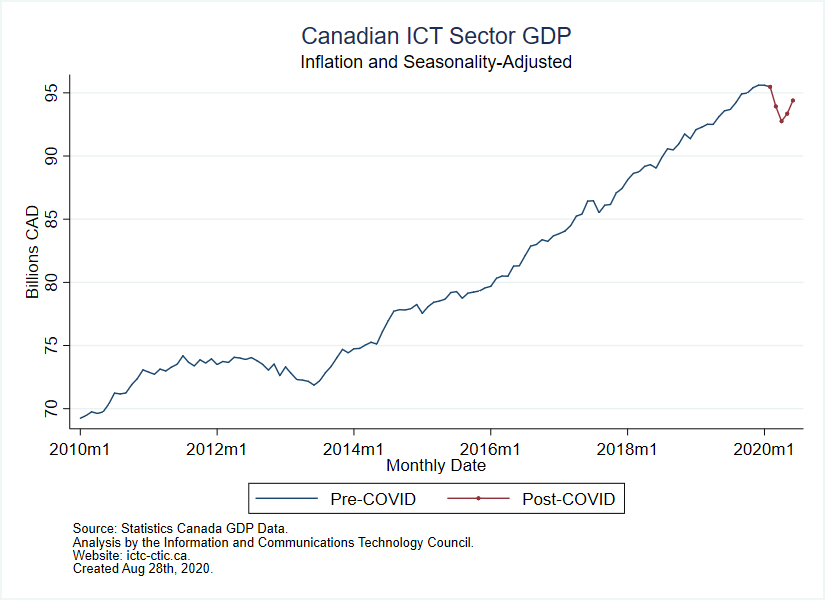

Most interestingly, Figure 5 showcases the remarkable anti-fragility of the Information and Communications Tech (ICT) sector GDP with respect to this crisis. As documented in ICTC’s just-released Revised Labour Market Outlook for 2022, ICT and the ‘Digital Economy’ have been nearly unscathed by the pandemic.

Figure 5: ICT GDP, Canada

Another sector that has proven relatively resilient is the recently liberalized Cannabis sector, which has grown in every month since the pandemic began, with economic activity reaching the manic exuberance of late last year (see Figure 6).

Figure 6: Cannabis Sector GDP, Canada. Reflects both legal and illegal activity, latter estimated by Statistics Canada.

The steep recovery in GDP in June does not, of course, preclude additional lock-downs, and reversals in economic fortune in the fall. Many viruses, including Coronaviruses like the “common cold” are seasonal. Indeed, the high probability of a “second wave” of infections in the fall appears to be the consensus view, for whatever that is worth.

On the other hand, there are reasons for continued optimism. Progress on vaccines has been remarkable, considering that a vaccine typically takes a decade to develop. Across the developed world, COVID-19 mortality rates have fallen sharply and somewhat mysteriously across all age brackets. This might be due to the accumulation of incremental knowledge on treatment, including avoiding intubation with a ventilator (early enthusiasm for ventilators may have been misplaced).

Coronavirus tests are falling in price and delivering faster responses, and researchers have come to better understand transmission mechanisms. Early in the pandemic, emphasis was placed on transmission via surface contact while masks were downplayed, the opposite of current wisdom. Notwithstanding sensationalist and moralizing journalist coverage of irresponsible “beach-goers,” it is understood that the virus does not transmit well outdoors or during brief encounters.

Statistics Canada’s June report gives Canadians the chance to breathe a sigh of relief. The crisis is far from over, but there are reasons for cautious optimism that the worst fears of a second “Great Depression” are less likely. Let us hope that progress continues to be made on the scientific basis of controlling the virus, including vaccines, treatments, and transmission, while Canadians return to work in the coming months.